Income Tax

★ Featured

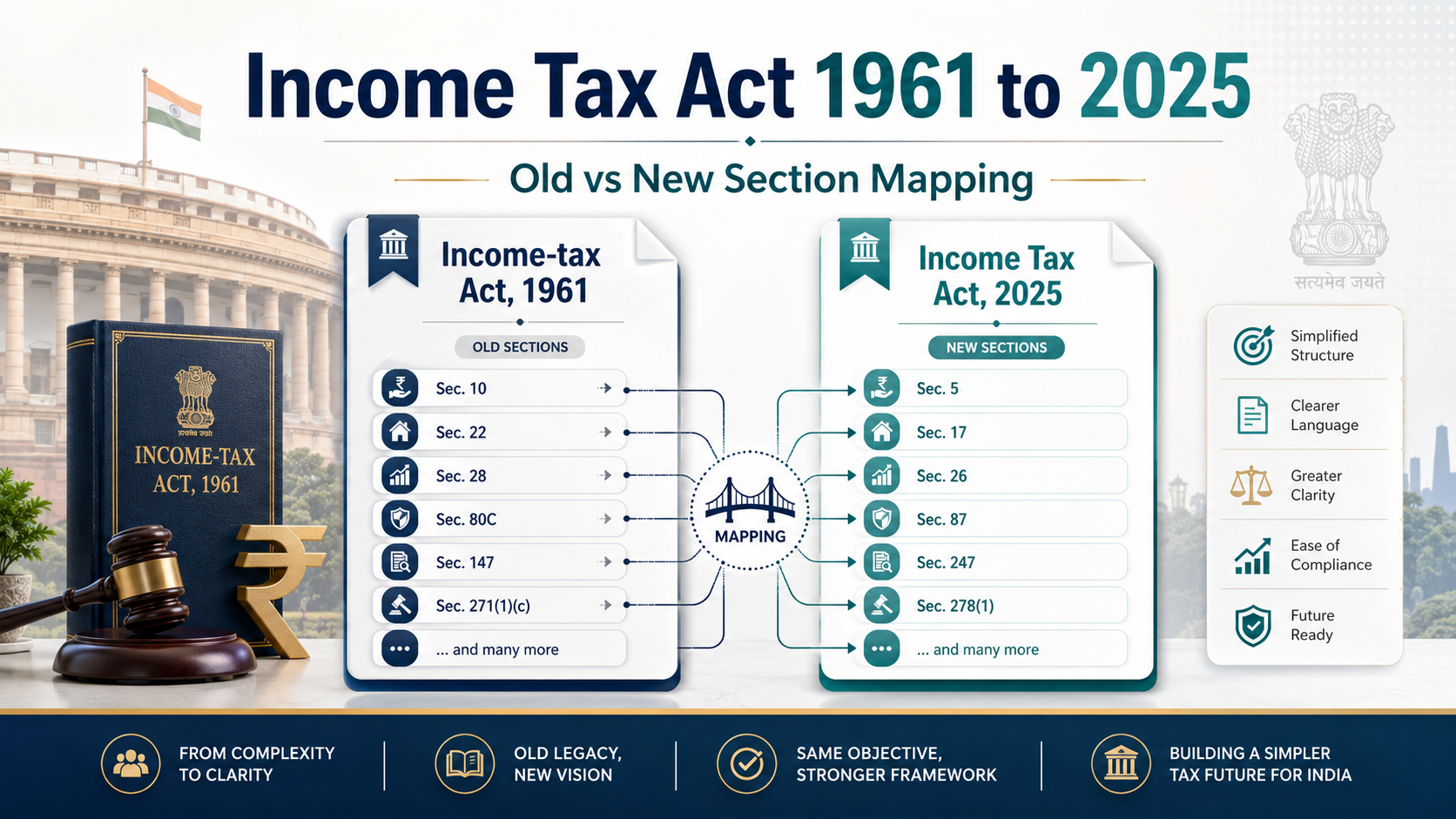

Income Tax Act 1961 to 2025 Section Mapping: Complete Old vs New Section Comparison

PSPG & Co LLP

14 May 2026

5 min read

Below is the old Income-tax Act, 1961 → new Income Tax Act, 2025 section mapping.

| Old Act section(s) — Income-tax Act, 1961 | New Act section(s) — Income Tax Act, 2025 | Provision / Topic |

|---|---|---|

| 1 | 1 | Short title, extent and commencement |

| 2 | 2 | Definitions |

| 3 | 3 | Definition of tax year |

| 4 | 4 | Charge of income-tax |

| 5 | 5 | Scope of total income |

| 6 | 6 | Residence in India |

| 7, 8 | 7 | Income deemed to be received / dividend deemed income |

| 9B | 8 | Receipt of capital asset or stock in trade by specified person |

| 9, 9A | 9 | Income deemed to accrue or arise in India |

| 5A | 10 | Portuguese Civil Code — apportionment between spouses |

| 10 | 11 | Incomes not included in total income |

| 13A, 13B | 12 | Income of political parties and electoral trusts |

| 14 | 13 | Heads of income |

| 14A | 14 | Expenditure relating to exempt income |

| 15 | 15 | Salaries |

| 17 | 16 | Income from salary |

| 17 | 17 | Perquisite |

| 17 | 18 | Profits in lieu of salary |

| 10(10), 10(10A), 10(10AA), 10(10B), 10(10C), 16 | 19 | Deductions from salaries |

| 22 | 20 | Income from house property |

| 23, 27 | 21 | Annual value |

| 24, 25 | 22 | Deductions from house property |

| 25A | 23 | Arrears of rent / unrealised rent |

| 26 | 24 | Property owned by co-owners |

| 27 | 25 | Interpretation — house property |

| 28 | 26 | Profits and gains of business or profession |

| 29 | 27 | Computing business/profession income |

| 30, 31, 38 | 28 | Rent, repairs, taxes, insurance |

| 36, 40A | 29 | Employee welfare deductions |

| 36 | 30 | Deduction on certain premium |

| 36 | 31 | Bad debt / doubtful debt |

| 36 | 32 | Other deductions |

| 32, 38 | 33 | Depreciation |

| 37 | 34 | General conditions for allowable deductions |

| 40 | 35 | Amounts not deductible |

| 40A | 36 | Expenses/payments not deductible in certain cases |

| 43B | 37 | Deductions allowed on actual payment basis |

| 41 | 38 | Deemed business profits |

| 43 | 39 | Actual cost |

| 43C | 40 | Cost of acquisition of certain assets |

| 43 | 41 | Written down value |

| 43A | 42 | Foreign exchange fluctuation — capitalisation |

| 43AA | 43 | Foreign exchange fluctuation — taxation |

| 35D | 44 | Preliminary expenses amortisation |

| 35 | 45 | Scientific research expenditure |

| 35AD | 46 | Capital expenditure of specified business |

| 35CCC, 35CCD | 47 | Agricultural extension / skill development |

| 33AB | 48 | Tea, coffee and rubber development account |

| 33ABA | 49 | Site Restoration Fund |

| 44A | 50 | Trade/profession association |

| 35E | 51 | Prospecting minerals expenditure |

| 35ABA, 35ABB, 35DD, 35DDA | 52 | Telecom, amalgamation, demerger, VRS etc. |

| 43CA | 53 | Transfer of assets other than capital assets |

| 42 | 54 | Mineral oil prospecting business |

| 44 | 55 | Insurance business |

| 43D | 56 | Interest income of specified financial institutions |

| 43CB | 57 | Revenue recognition for construction/service contracts |

| 44AD, 44ADA, 44AE | 58 | Presumptive taxation for certain residents |

| 44DA | 59 | Royalty / fees for technical services of non-residents |

| 44C | 60 | Head office expenditure of non-residents |

| 44B, 44BB, 44BBA, 44BBB, 44BBC, 44BBD | 61 | Presumptive income of certain non-residents |

| 44AA | 62 | Maintenance of books of account |

| 44AB | 63 | Tax audit |

| 44DB | 64 | Business reorganisation of co-operative banks |

| 44DB | 65 | Interpretation for section 64 |

| 28 to 44DA | 66 | Interpretation — business/profession income |

| 45 | 67 | Capital gains |

| 46 | 68 | Distribution of assets by companies in liquidation |

| 46A | 69 | Buy-back of shares/securities |

| 47 | 70 | Transactions not regarded as transfer |

| 47A | 71 | Withdrawal of exemption |

| 48 | 72 | Computation of capital gains |

| 49 | 73 | Cost with reference to certain modes of acquisition |

| 50 | 74 | Capital gains for depreciable assets |

| 50A | 75 | Cost of acquisition for depreciable assets |

| 50AA | 76 | Market Linked Debenture |

| 50B | 77 | Slump sale |

| 50C | 78 | Full value of consideration in certain cases |

| 50CA | 79 | Unquoted shares |

| 50D | 80 | FMV deemed full value of consideration |

| 51 | 81 | Advance money received |

| 54 | 82 | Sale of residential house |

| 54B | 83 | Agricultural land |

| 54D | 84 | Compulsory acquisition of land/building |

| 54EC | 85 | Investment in specified bonds |

| 54F | 86 | Investment in residential house |

| 54G | 87 | Shifting industrial undertaking from urban area |

| 54GA | 88 | Shifting industrial undertaking to SEZ |

| 54H | 89 | Extension of time for acquiring/investing capital gains |

| 55 | 90 | Cost of improvement / acquisition |

| 55A | 91 | Reference to Valuation Officer |

| 56 | 92 | Income from other sources |

| 57 | 93 | Deductions from other sources |

| 58 | 94 | Amounts not deductible |

| 59 | 95 | Profits chargeable to tax |

| 60 | 96 | Transfer of income without transfer of assets |

| 61, 62 | 97 | Revocable transfer of assets |

| 63 | 98 | “Transfer” and “revocable transfer” defined |

| 64 | 99 | Clubbing income of spouse, minor child etc. |

| 65 | 100 | Liability where income included in another person’s income |

| 66 | 101 | Total income |

| 68 | 102 | Unexplained credits |

| 69, 69B | 103 | Unexplained investment |

| 69A, 69B | 104 | Unexplained asset |

| 69C | 105 | Unexplained expenditure |

| 69D | 106 | Borrowing/repayment through hundi etc. |

| 70 | 108 | Set-off of losses under same head |

| 71 | 109 | Set-off of losses under another head |

| 71B | 110 | House property loss |

| 74 | 111 | Capital gains loss |

| 72 | 112 | Business loss |

| 73 | 113 | Speculation business loss |

| 73A | 114 | Specified business loss |

| 74A | 115 | Specified activity loss |

| 72A | 116 | Accumulated losses / depreciation in amalgamation or demerger |

| 72AA | 117 | Amalgamation in certain cases |

| 72AB | 118 | Business reorganisation of co-operative banks |

| 78, 79 | 119 | Carry forward and set-off not permissible |

| 79A | 120 | No set-off against undisclosed income |

| 80 | 121 | Submission of return for losses |

| 80A, 80AB, 80AC, 80B | 122 | General deduction rules |

| 80C, 80CCC, 80CCE | 123 | Life insurance, PF, deferred annuity etc. |

| 80CCD | 124 | Pension scheme contribution |

| 80CCH | 125 | Agnipath Scheme contribution |

| 80D | 126 | Health insurance premium |

| 80DD | 127 | Dependant with disability |

| 80DDB | 128 | Medical treatment |

| 80E | 129 | Higher education loan interest |

| 80EE | 130 | Residential house property loan interest |

| 80EEA | 131 | Certain house property loan interest |

| 80EEB | 132 | Electric vehicle loan interest |

| 80G | 133 | Donations to funds/charitable institutions |

| 80GG | 134 | Rent paid |

| 80GGA | 135 | Donations for scientific research / rural development |

| 80GGB | 136 | Company contributions to political parties |

| 80GGC | 137 | Contributions to political parties by any person |

| 80-IA | 138 | Infrastructure undertakings |

| 80-IAB | 139 | SEZ development |

| 80-IAC | 140 | Specified business |

| 80-IB | 141 | Certain industrial undertakings |

| 80-IBA | 142 | Housing projects |

| 80-IE | 143 | Undertakings in North-Eastern States |

| 10AA | 144 | Newly established SEZ units |

| 80JJA | 145 | Bio-degradable waste business |

| 80JJAA | 146 | Additional employee cost |

| 80LA | 147 | Offshore Banking Units / IFSC units |

| 80M | 148 | Inter-corporate dividends |

| 80P | 149 | Co-operative societies |

| 80P | 150 | Interpretation for section 149 |

| 80QQB | 151 | Royalty income of authors |

| 80RRB | 152 | Royalty on patents |

| 80TTA, 80TTB | 153 | Interest on deposits |

| 80U | 154 | Person with disability |

| 87 | 155 | Rebate in computing income-tax |

| 87A | 156 | Rebate for certain individuals |

| 89 | 157 | Salary arrears/advance relief |

| 89A | 158 | Retirement benefit account in notified country |

| 90, 90A | 159 | Double taxation agreements |

| 91 | 160 | Countries with no agreement |

| 139A, 139AA | 262 | Permanent Account Number |

| 139, 139D, 194P | 263 | Return of income |

| 139B | 264 | Tax return preparers |

| 140 | 265 | Return verification |

| 140A | 266 | Self-assessment |

| 140B | 267 | Updated return tax |

Have Questions? We're Here to Help

Get expert advice from PSPG & Co LLP. Reach out to discuss your requirements.

Tags:

#Income Tax Act 2025

#Income Tax Act 1961

#Old vs New Tax Act

#Section Mapping

#Income Tax Sections

#New Income Tax Law

#Indian Tax Law

#Tax Compliance

#Income Tax Updates

#Direct Tax Reform

#Tax Professionals

#Income Tax India

#