ITR Filing Deadlines for FY 2025-26: Dates, Missed Deadlines, Penalties and What Taxpayers Should Do Next

For most taxpayers, income tax return filing feels like a once-a-year formality. But the real problem begins when the due date is missed, the wrong ITR form is selected, or an error is discovered after submission. A delay of even a few weeks can lead to late fees, interest, loss of certain tax benefits, and unnecessary stress during loan, visa, or financial verification processes.

For FY 2025-26, relevant to AY 2026-27, taxpayers need to be especially careful because different return forms and taxpayer categories now carry different filing timelines. The old habit of assuming that “31st July is the deadline for everyone” can easily lead to mistakes.

Why the ITR Due Date Matters

The ITR deadline is not just a compliance date. It affects your ability to revise mistakes, carry forward losses, avoid late filing fees, and keep your tax record clean. For salaried individuals, freelancers, professionals, business owners, and taxpayers with capital gains, missing the correct deadline can have different consequences.

A timely filed return gives you more control. A late return limits your options.

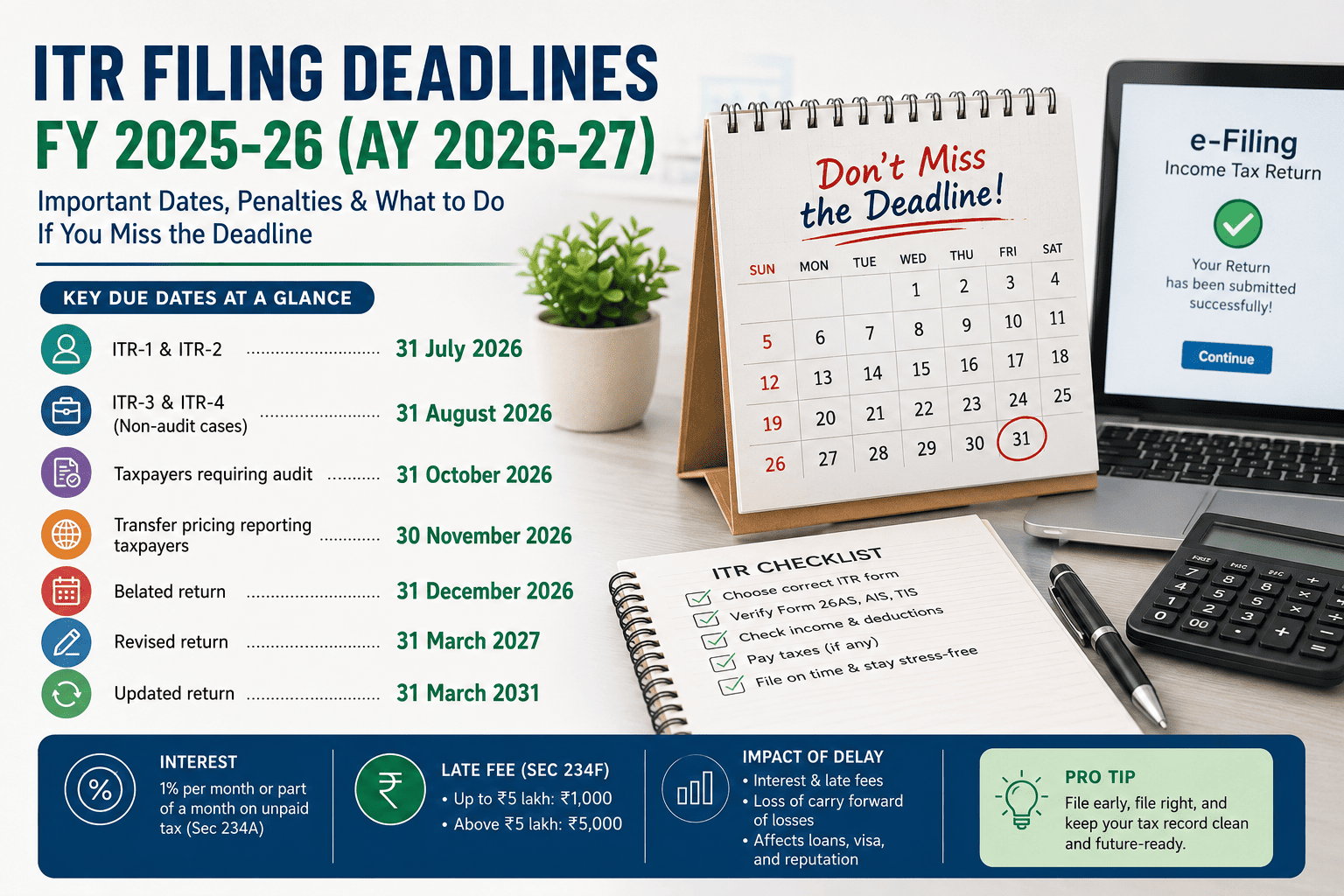

ITR Filing Due Dates for FY 2025-26 / AY 2026-27

For taxpayers not covered under tax audit, the applicable due date depends on the ITR form.

| Taxpayer / Return Category | Due Date |

|---|---|

| ITR-1 and ITR-2 | 31 July 2026 |

| ITR-3 and ITR-4, non-audit cases | 31 August 2026 |

| Taxpayers requiring audit | 31 October 2026 |

| Taxpayers covered under transfer pricing reporting | 30 November 2026 |

| Belated return | 31 December 2026 |

| Revised return | 31 March 2027 |

| Updated return | 31 March 2031 |

This distinction is important. Many taxpayers with business income, professional income, presumptive taxation, or partnership-related income may fall under ITR-3 or ITR-4. For such non-audit cases, the due date is 31 August 2026, not 31 July 2026.

What Happens If You Miss the Original Due Date?

Missing the original ITR deadline does not mean the return can no longer be filed. The Income Tax Act allows a taxpayer to file a belated return.

For FY 2025-26, a belated return can be filed up to 31 December 2026.

However, filing late comes with costs. You may have to pay interest, late filing fees, and you may lose the right to carry forward certain losses.

Think of a belated return as a second chance, not a free extension.

Belated Return vs Updated Return

Taxpayers often confuse belated returns with updated returns. Both are used when the normal filing window has been missed, but they serve different purposes.

A belated return is used when you missed the original due date but are still filing within the belated return window. For AY 2026-27, that window closes on 31 December 2026.

An updated return is a later correction mechanism. It can be filed even after the belated return deadline has passed, within the permitted extended period. For FY 2025-26, the updated return window extends up to 31 March 2031.

But there is one major limitation: an updated return is not meant to claim fresh benefits or reduce your tax liability. It is generally used to disclose additional income or correct omissions where additional tax may be payable.

What If You Filed Your ITR but Later Found a Mistake?

This is more common than most taxpayers admit. A deduction may be missed. A bank interest figure may be left out. A capital gain may be wrongly reported. Sometimes Form 26AS, AIS, and the return filed do not match properly.

In such cases, the solution is a revised return.

For FY 2025-26, the revised return can be filed up to 31 March 2027.

For example, suppose a taxpayer files the original return in June 2026 and later realises that an eligible deduction was not claimed. The return can be revised before the revised return deadline, provided the correction is made within the permitted time.

A revised return is valuable because it allows taxpayers to fix genuine mistakes while the filing year is still open.

Interest for Late Filing

If tax remains unpaid and the return is filed after the due date, interest may apply under Section 234A of the Income Tax Act, 1961.

The interest is generally calculated at 1% per month or part of a month on the unpaid tax amount.

This means even a delay of a few days into the next month can count as a full month for interest calculation. Taxpayers who have self-assessment tax payable should therefore avoid waiting until the last moment.

Late Filing Fee Under Section 234F

Apart from interest, late filing fees may also apply.

The fee can be:

| Total Income | Late Filing Fee |

|---|---|

| Up to ₹5 lakh | ₹1,000 |

| Above ₹5 lakh | ₹5,000 |

This fee is separate from interest. So, a taxpayer may end up paying both late fee and interest if tax is unpaid and the return is filed after the due date.

Loss of Carry Forward Benefit

One of the most serious consequences of missing the original due date is the loss of carry forward of certain losses.

This is especially relevant for taxpayers having:

Capital loss from shares, mutual funds, property, or other assets

Business loss

Speculative or trading-related losses, where applicable

If the return is not filed within the original due date, such losses may not be allowed to be carried forward to future years.

This can hurt taxpayers who had a bad investment year or business loss and were hoping to adjust those losses against future gains.

Why Late ITR Filing Can Affect More Than Tax

Delayed return filing may also create practical problems outside the income tax portal.

Banks often ask for ITRs while processing loans. Visa authorities may consider tax returns while checking financial credibility. Some tenders, business registrations, financial applications, and professional documentation also require properly filed returns.

A late-filed return may not automatically disqualify you, but it can create avoidable questions.

In financial compliance, timing creates credibility.

Income Tax Act 1961 and Income Tax Act 2025: Which Law Applies?

Although the Income Tax Act, 2025 takes effect from 1 April 2026, AY 2026-27 relates to income earned during FY 2025-26, that is, income earned up to 31 March 2026. Therefore, the provisions of the Income Tax Act, 1961 continue to remain relevant for this assessment year.

For reference, some corresponding provisions are:

| Topic | Income Tax Act, 1961 | Income Tax Act, 2025 |

|---|---|---|

| Interest for late or non-filing | Section 234A | Section 423 |

| Late filing fee | Section 234F | Section 428 |

| Belated return | Section 139(4) | Section 263(4) |

| Revised return | Section 139(5) | Section 263(5) |

Taxpayers and professionals should be careful while reading older and newer references, because the applicable law may depend on the assessment year involved.

Practical Filing Checklist for Taxpayers

Before filing the return, taxpayers should check:

Whether the correct ITR form is being used

Whether Form 16, Form 26AS, AIS, and TIS have been matched

Whether bank interest, capital gains, foreign income, and other income have been properly reported

Whether deductions and exemptions have been correctly claimed

Whether self-assessment tax, if any, has been paid before filing

Whether business or capital losses need to be carried forward

A return filed in a hurry may later need revision. A return filed after the due date may cost money. A return not filed at all may create bigger problems.

Final Takeaway

For FY 2025-26, ITR filing should not be treated as a last-week activity. The correct deadline depends on the taxpayer category and ITR form. For ITR-1 and ITR-2, the due date is 31 July 2026. For non-audit ITR-3 and ITR-4 cases, the due date is 31 August 2026. Audit and transfer pricing cases have later deadlines.

If you miss the original date, a belated return can still be filed by 31 December 2026. If you discover an error, a revised return can be filed by 31 March 2027. If both windows are missed, an updated return may still be possible, but with limitations.

The safest approach is simple: file early, verify carefully, and correct mistakes before the window closes. In tax compliance, delay rarely helps — but timely action almost always does.

Have Questions? We're Here to Help

Get expert advice from PSPG & Co LLP. Reach out to discuss your requirements.